In 2024, Lithuanian investment transactions market slumped by 43%

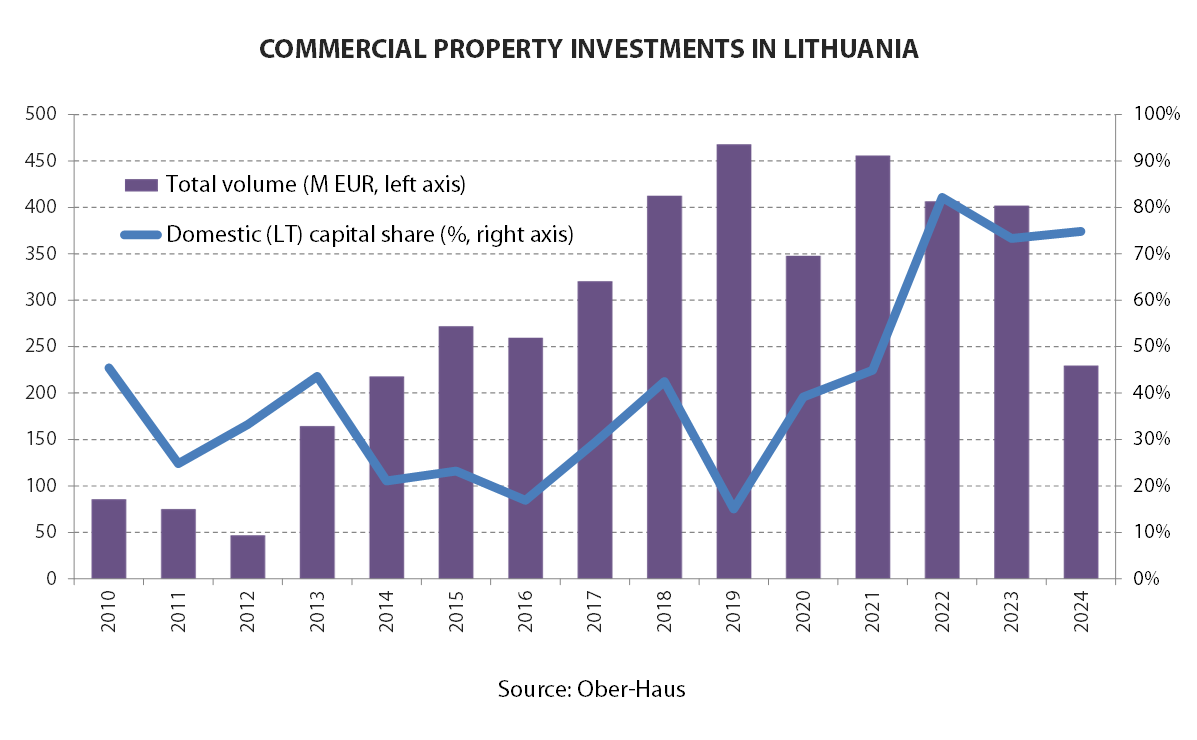

The general sentiment in the Lithuanian commercial property market in 2024 is well reflected in the volume of investments, which has declined to the levels last seen in 2014. According to the data of Ober-Haus, in 2024, the value of modern cash-flow commercial property (modern office, retail and industrial objects with the value of at least EUR 1.5 million) acquired amounted to EUR 230 million. This means that the annual volume of investments declined by 43% compared to 2023 or 2022.

‘In 2024, only small and medium-sized transactions were recorded in Lithuania, whereas there had been no acquisitions of larger transactions at all. For the first time after a lengthy period, the value of the largest deal did not exceed EUR 30 million‘, said Raimondas Reginis, head of market research for the Baltics at Ober-Haus. According to Ober-Haus, deals up to EUR 10 million in value represented 40% of total investments in Lithuania, whereas deals valued at EUR 10–30 million – the rest (60%).

Retail properties attracted the largest share of investments, with investors primarily focusing on supermarkets

The largest portion of investments befell to retail properties with EUR 134 million or 58% of all investments in commercial property in Lithuania spent for acquisitions. In 2024, this segment was noted for the most significant acquisitions as well as the biggest number of deals.

For example, a fund managed by Estonian company Eften Capital purchased Una retail park, opened in the middle of 2023, at the northern part of Vilnius (nearby Molėtų Road). In the meantime, a fund of Latvian investment management company, Provendi Asset Management, bought in Panevėžys the DYI shopping centre of the construction materials and household products chain Depo. Besides these larger transactions, in the retail segment, buyers were especially actively seeking small-format supermarkets (1,500–2,500 sqm), operated by the major grocery store chains. During 2024, as many as 10 objects of such format were purchased, while the largest transaction involved the sales of four newly constructed Lidl stores to a fund managed by the investment management company, DIFF Assets.

‘Broad geographical distribution also suggests that this kind of property remains particularly attractive to investors. Stores were purchased in the largest cities as well as in smaller towns of the country: Panevėžys, Molėtai, Alytus, Marijampolė, Prienai, Jurbarkas, and Vilnius and Klaipėda districts. This indicates that investors trust in the continued success of their tenants’ operations in such properties and are paying record-high prices for them, even during a period of weak market activity’, Mr Reginis said.

In 2024, office segment attracted EUR 70 million in investment

The second largest share of investments in 2024 went to the segment of office premises, with EUR 70 million spent or 31% of total investment in commercial property made in Lithuania.

The largest transaction in the office segment was concluded in the second half of the year, when the sale of a complex of administrative buildings on A. Juozapavičiaus Street and Žvejų Street in Vilnius was announced. Buildings with 16,000 sqm of floor space and a land plot in the central part of the city were bought by the real estate developer Realco, which sees new development opportunities in this area. In the middle of 2024, a fund of investment management company ZeroSum Asset Management purchased a complex of three office buildings from the Norwegian capital company AMG Property in Švitrigailos Street, in Vilnius. In the meantime, at the beginning of the year, a real estate development company Eriadas together with the closed-end investment fund for informed investors DIFF Develop acquired the buildings of the insurance company Ergo in Geležinio Vilko Street, in Vilnius.

‘The number of investment deals made and prices of property acquired in the recent years suggest that investors are still wary of the office segment. The slowing expansion of the business and growing level of vacant office premises reduced the attractiveness of this segment and led the investors to approach the assessments of this real estate segment more conservatively’, Mr Reginis explained. This is particularly the case in the capital city of the country, where office development has not stopped and the vacancy rate of premises over the last two years hopped from 5.9% to 8.8%, while the total area of vacant premises for the first time in history exceeded 100,000 sqm.

The remaining (11%) smallest share of investments traditionally went to the acquisition of warehousing and manufacturing premises. The largest deal of 2024 was concluded in Kaunas, where the fund of the investment company Eika Asset Management sold a 5,600 sqm logistics building to its tenant, Camelia pharmacy chain. Other smaller acquisitions were carried out in Vilnius and Kaunas and Klaipėda regions.

Local capital continues dominating the investment market

The most recent annual data suggest that local capital retains its predominant position in the commercial real estate transactions’ market. Sharp growth of local capital investments share recorded in the Lithuanian investment transactions’ market since 2022 remained at record high in 2024, too. According to Ober-Haus data, in 2022, the share of capital held by Lithuanians in investment transactions shot to 82%, in 2023 accounted for 73%, and in 2024 – for 75%. ‘For instance, over the period of 2012–2021, the share of local investors comprised 37% in total investments. This suggests that foreign investors have not yet returned to our country’s real estate market, and currently, only investors from other Baltic States – Latvia and Estonia – are interested in investing’, the analyst said.

More positive changes can finally be expected after a deep fall

Recent prices of commercial real estate suggest that there is still a wide variation in prices, both across individual segments and in terms of the quality of the properties. According to Mr Reginis, buyers are especially cautious about the prospects – potential lease revenues and likely additional investments – of older objects and those located in smaller towns of the country. Consequently, they seek to acquire such objects with the maximum yield possible that might even reach double figures (e.g. 10–11%). ‘In the meantime, new objects in the capital or strategically attractive locations of other cities receive greater interest from the buyers. Fully occupied objects guarantee for the buyers an indexed cash flow and minimum investments to the object maintenance in the medium or lengthier period; hence, such objects even now can be acquired with a 6.5–7.0% yield. Smaller objects, such as stand-alone supermarkets, can be bought with a yield slightly below 6.0%’, the representative of Ober-Haus explained.

In view of the overall situation in the commercial real estate market and specifically in the investment transactions’ market in 2024, more positive developments can be expended in 2025.

‘Irrespective of the persisting geopolitical tensions, the growing economy of the country and decreasing interest rates might enliven the business (tenants) expansion and boost up the overall activity of the commercial real estate market – in particular, in the segment of office or warehousing premises. For instance, as of the middle of 2024, clear positive trends have been seen in the housing market. This would enhance the investor confidence in the commercial real estate market, and higher activity could be expected in the investment transactions’ market as well. We are unlikely to see a more active return of foreign investors to our market; however, local investors should act with more courage’, Mr Reginis said.

Latest news

In 2024, Lithuanian investment transactions…

The general sentiment in the Lithuanian commercial property market in…

Ober-Haus completes the sale of…

A. Juozapavičiaus Street, Kaunas, the last apartment in the project…

In 2024, annual apartment price…

The Ober-Haus Lithuanian apartment price index (OHBI), which follows changes…